Given the huge innovation in payment initiation for consumers its only a matter of time that businesses would ask banks what options are available for them to participate in the instant payment world.

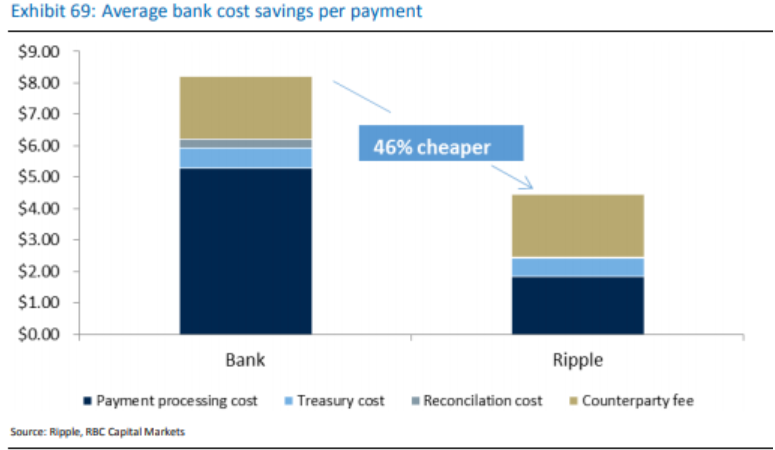

Its not going to be easy for banks. They will have to take calls that may or may not pan out. One area they can start thinking about is the Clearing and Settlement function. There is a history of lag and costs in this area. However there is sporadic innovation as well. Ripple's cross border RippleNet system has shown the potential for reducing costs in Cross Border clearing and settlement. Swift GPI is showing a method to introduce transparency and tracking in cross border payment flows.

But these are technology based offerings. Regulators in many countries are encouraging development of new instant payment rails such as IMPS in India . China, Japan, Australia, Canada, USA and lastly EU have plans to set up these rails and are various points in their rollout.

By taking calls on which technology to utilize and what networks to participate in , banks can offer differentiated clearing and settlement-- based on countries they want to focus on, speed of settlement, transparency of payment journey, SLA based straight through processing STP to name a few.

However the table stakes in all these offerings will be an end to end ISO20022 message compliant network